Will ocean rates collapse?

Demand is being pulled forward, ships are being built, and the Red Sea may reopen. The post Will ocean rates collapse? appeared first on FreightWaves.

Ocean demand being pulled forward

The main debate regarding the container ship market is whether several factors will converge to tank rates later this year. Most industry professionals are on board with the view that there was a significant pull forward of imports to avoid tariffs and potential port worker labor strife. According to Global Port Tracker, port activity increased 14.4% and 14.8% for December and all of 2024, respectively. Imports at the Port of Los Angeles have also been tracking about 15% above normal seasonal levels.

Despite the strong volume in the past year, Global Port Tracker does not expect a major falloff in volume during the first half of the year. Its expected y/y changes in twenty-foot equivalent unit port volume is 7.8% in January (data not yet released), 0.2% in February, 11.1% in March, 8.2% in April, 5.4% in May and -0.6% in June. (See article here for detail.)

If those forecasts are in the ballpark of accuracy, the questions then become: What happens to ocean demand in the second half, and is there still a pull forward with a 10% tariff on China? After all, Trump has described 10% as “just an opening salvo.” Plus, tariffs are likely to be imposed on a wider group of countries soon, such as Japan and those in the European Union. On top of tariffs, European consumers are generally not in as good a position as American consumers because their inflation has been even worse.

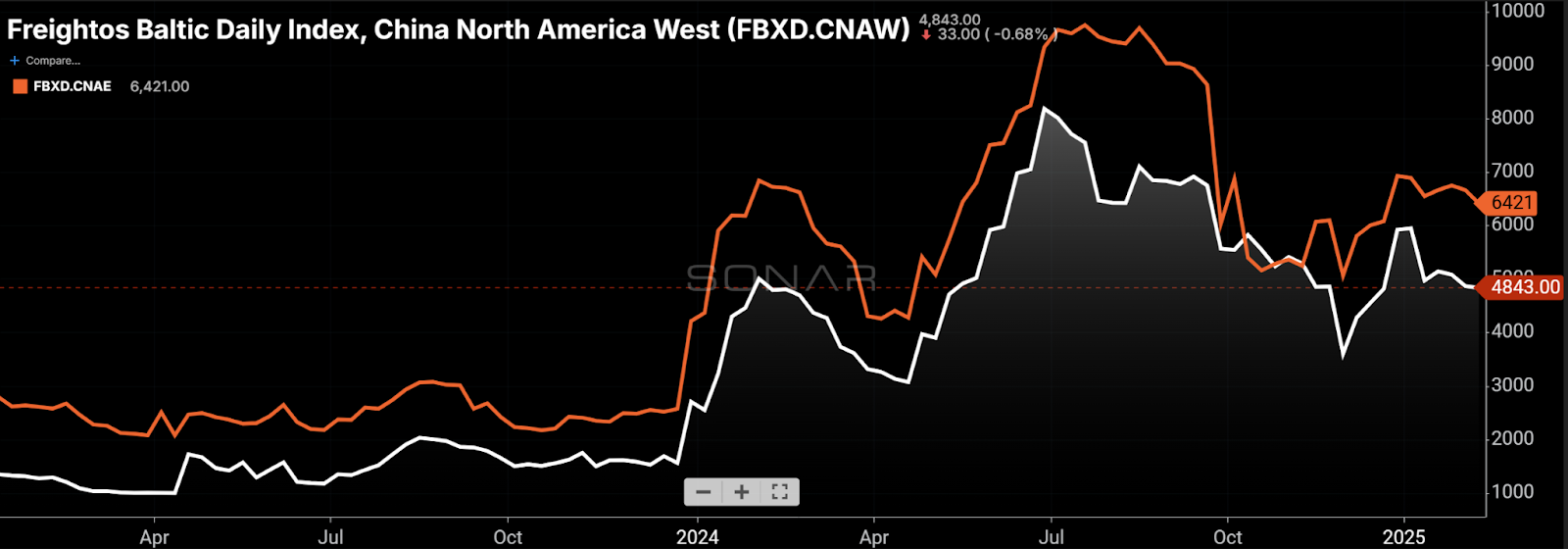

Global Port Tracker expects 2025 port activity to compare favorably with 2024 through at least the first half of the year before year-ago comparisons get more difficult. The chart above presents an index of U.S. import bookings taken at the point of overseas origin. (Chart: SONAR)

Ocean capacity is increasing

Earlier this week, journalist Stuart Chirls wrote my favorite FreightWaves headline in a long time, giving some reasons why container rates may hold up in the near term. One reason is the demand forecast highlighted above. Another is that it’s not a certainty that carriers will rush back to the Red Sea given the region’s risk and also the tremendous positive impact that avoiding the region had on carriers’ profitability. If collusion were possible, carriers might agree to never use the Red Sea for intercontinental movements again, but in a competitive market, containers can be moved more cost-effectively (Flexport estimates $400-$500 less per container, on average) with far faster service through the Suez Canal.

The ceasefire seems tenuous and the region is risky, but if carriers fully return to the Red Sea, it would meaningfully increase ocean capacity, which could then exceed demand. On a recent webinar, Flexport estimated that the longer routings around the Cape of Good Hope removed 8%-10% of capacity from the ocean market, and a return would put the container ship market in an overcapacity position. Opinions on when carriers will fully return to the Red Sea differ. While the head of the Suez Canal expects vessel traffic to return to normal by late March and fully recover by the end of this year, the head of a major container line said he doesn’t think carriers will restart scheduled services until May at the earliest. (See article here.)

The Red Sea impact could come on top of the impact from shipbuilding. On a recent webinar, Flexport estimated that, given shipbuilding schedules, 8% incremental capacity will come into the industry in 2025 and an additional 6% in 2026. Worth noting: Not all capacity is fungible, and the new capacity will mainly be for larger vessels that can only call on certain ports.

Spot rates to move containers from China to the U.S. are currently around early 2024 levels, the period shortly after the Red Sea attacks began. Carriers may blank sailings in an effort to stabilize rates, which may come under pressure later this year. (Chart: SONAR)

That said, there are factors that could mitigate a major rise in effective capacity. As seasonal strong periods approach, the industry could see the return of port congestion. Last year, ocean spot rates took an unexpected jump in the middle of the year due largely to congestion in certain key locations like the Port of Singapore. Plus, ocean carriers will likely blank sailings and adjust schedules in an effort to keep rates stable.

The Stockout show: De minimis exemption remains in place for now

(Photo: FWTV)

On Monday’s The Stockout show, I discussed the de minimis exemption, CPG ingredient prices and the freight markets.

While the elimination of the de minimis exemption was delayed to allow time to implement enforcement procedures, it remains likely that the exemption will be removed, with major implications for retailers and freight markets. At $800, the U.S. has a tariff exemption that is unusually high and, according to the House Select Committee, Shein and Temu are responsible for more than 30% of inbound U.S. de minimis shipments.

An elimination of the exemption would level the playing field with other retailers such as Gap and H&M, which paid $700 million and $205 million in import duties in 2022 while Shein and Temu paid nothing. The Chinese sellers may rethink their entire made-to-order strategy. It also may lead to a normalization in air cargo rates, which have remained well above pre-pandemic levels. A potential drop in the volume of cheap e-commerce imports could spur a change in parcel carriers’ volume and mix; in recent quarters, the bulk of UPS’ growth has come from low-value and low-service offerings, some of which it is planning to de-market.

Watch Monday’s show here and check out the full The Stockout playlist here.

Cocoa prices pressure CPG earnings

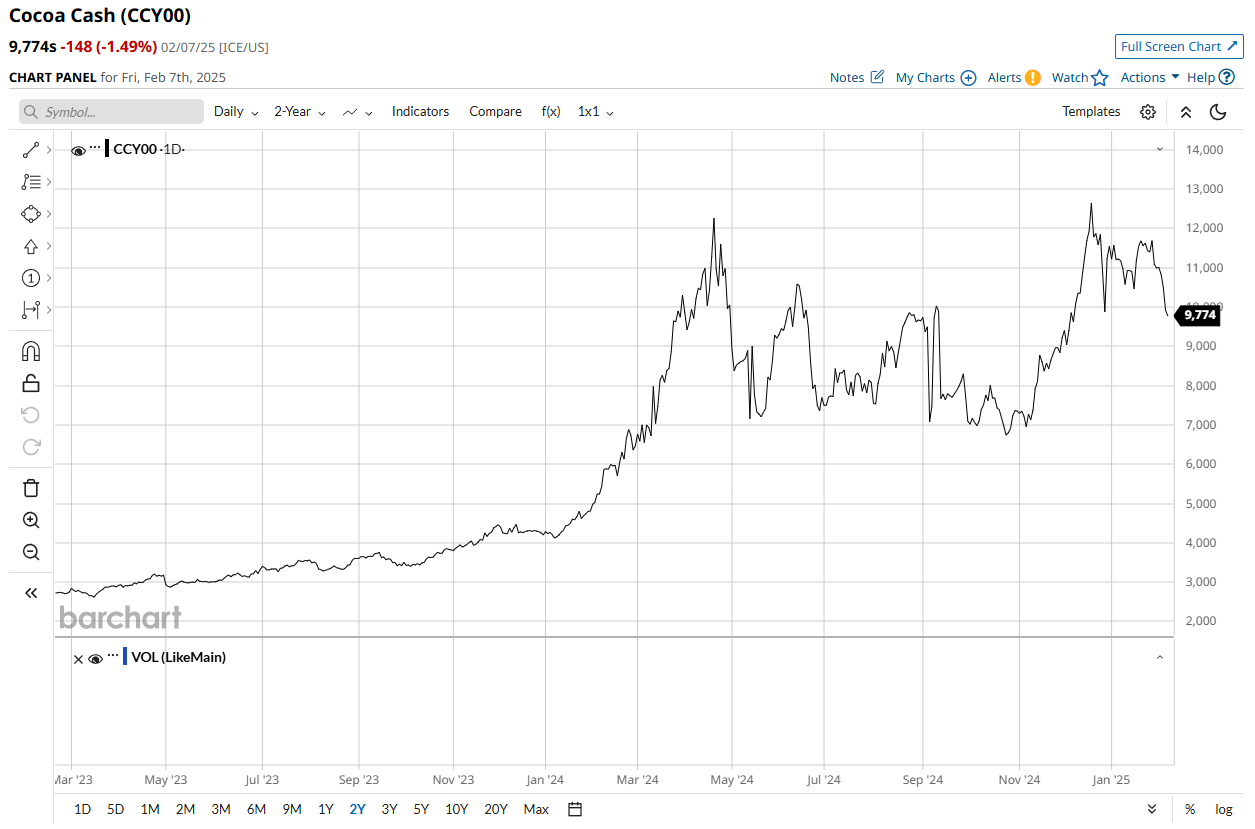

(Chart: Barchart.com Inc.)

Due to adverse growing conditions in Ghana and the Ivory Coast, cocoa prices have surged since late 2023 and, while off their highs, remain more than twice as high as they were a year and a half ago.

Snacking giants Hershey’s and Mondelez have both guided analysts lower as a result of inflation in cocoa and other ingredients, such as sugar. Hershey’s expects its adjusted gross margin to contract 650-700 basis points this year with a 40% decline in earnings per share despite net sales growth of at least 2%. Mondelez is more diversified with snacks outside of chocolate but still expects a 10% decline in adjusted earnings per share this year due to ingredient inflation.

CPG companies often hedge with forward contracts but can only mitigate that risk for so long. Plus, they generally need to honor near-term price agreements with retailers. In response to the ingredient inflation, Hershey’s plans to adjust pricing, packing architecture, and even formulations and investment strategies. The chocolate giant also faces risks from GLP-1 drugs inhibiting cravings – management concedes that they are having a “mild impact” on sales.

The post Will ocean rates collapse? appeared first on FreightWaves.