Another year of stagnant intermodal pricing?

Freight market not tightening in time for bid season. The post Another year of stagnant intermodal pricing? appeared first on FreightWaves.

Intermodal rates mixed across lanes

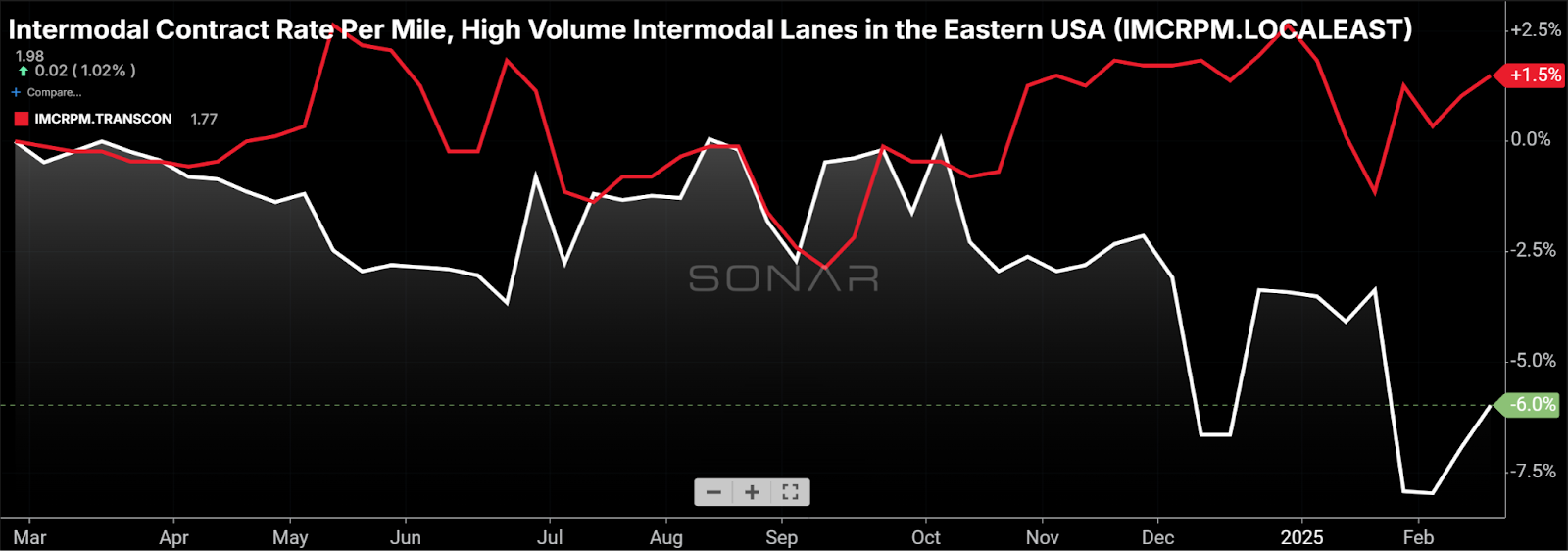

The one-year change in the Transcon Index and the Local East Index are shown in red and white, respectively. (Chart: SONAR)

Late last year, SONAR rolled out intermodal contract rates by lane. These include fuel surcharges. In addition to lane-level rates for 67 lanes, SONAR includes a Transcon Index (IMCRPM.TRANSCON – red line above) and a Local East (IMCRPM.LOCALEAST – white line above) Index. Detail on the components of those indexes is available here.

A trend has emerged in comparing the year-over-year changes between the two indexes versus year-ago levels. The Transcon Index is up 1.5% while the Local East Index is down 6%. While the intermodal industry is not close to being fully through bid season, the pattern appears consistent with what the domestic intermodal carriers said on their fourth-quarter earnings calls. They guided to rising rates on headhaul lanes – the Transcon Index is an average of five headhaul lanes outbound from LA – but also suggested that may not be the case on backhaul lanes or lanes where they may price to improve network balance. (The Local East Index represents a combination of headhaul and backhaul lanes.) What’s also different between transcon and local east intermodal lanes is that the latter group is more competitive with truckload. Despite optimism among carriers and analysts that truckload pricing will inflect to the upside this year, SONAR data does not yet show that translating to upward pressure on intermodal contract rates in modally competitive lanes.

Ocean spot rates mixed by lane

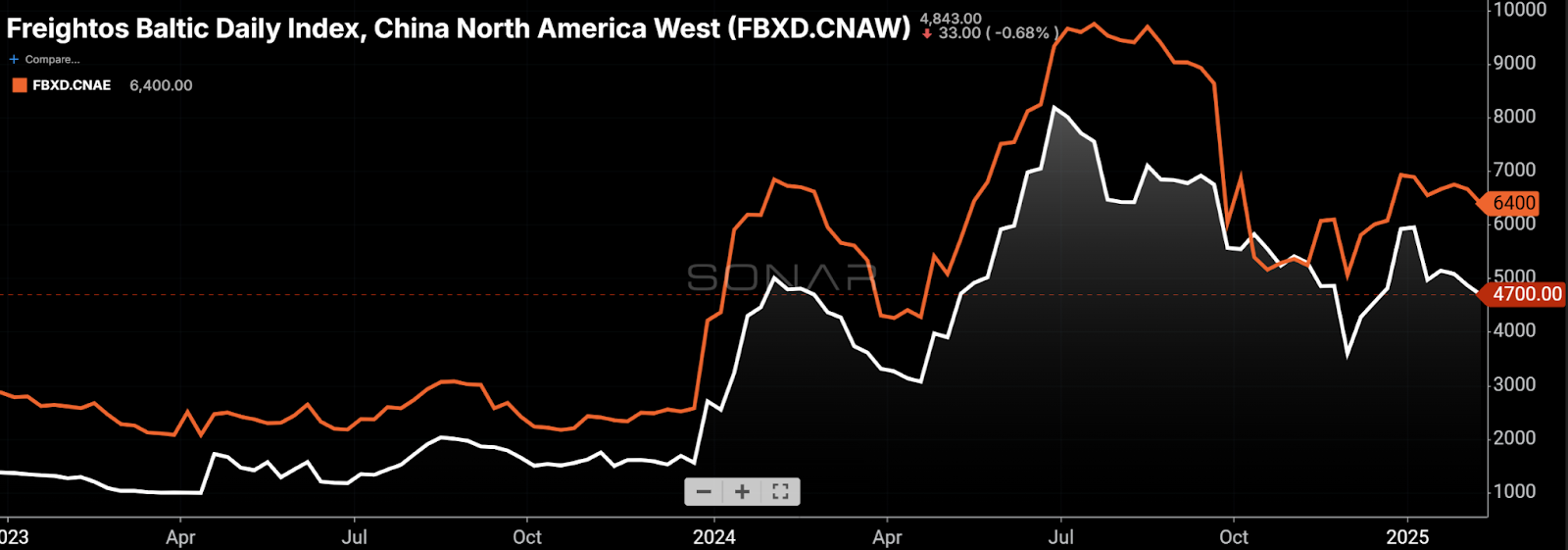

(Chart: SONAR)

Last fall, container ship spot rates from China to the U.S. East Coast and spot rates from China to the U.S. West Coast were roughly at parity. That was unusual and out of step with the extra cost of the one-and-a-half- to two-week additional sailing time associated with the longer routing to the East Coast. The latest data shows the spread expanding to $1,700, or above the historic average of about $1,000.

The longer ocean routing to the East Coast, while more costly on the ocean, is more economical for goods terminating on the East Coast when lower surface transportation costs are also considered. So, the rising spread suggests that a large portion of U.S. imports are currently not time-sensitive, which likely reflects a combination of seasonality and the potential for even higher tariffs on China since the recent 10% incremental tariff is supposedly just an “opening salvo.” The rising spread suggests a shift in demand toward all-water routes to the East Coast, and those routings are less conducive to rail intermodal. However, the evidence of lack of time sensitivity suggests that many of the imports hitting the West Coast ports will be very compatible with intermodal networks, which should build on recent intermodal volume strength.

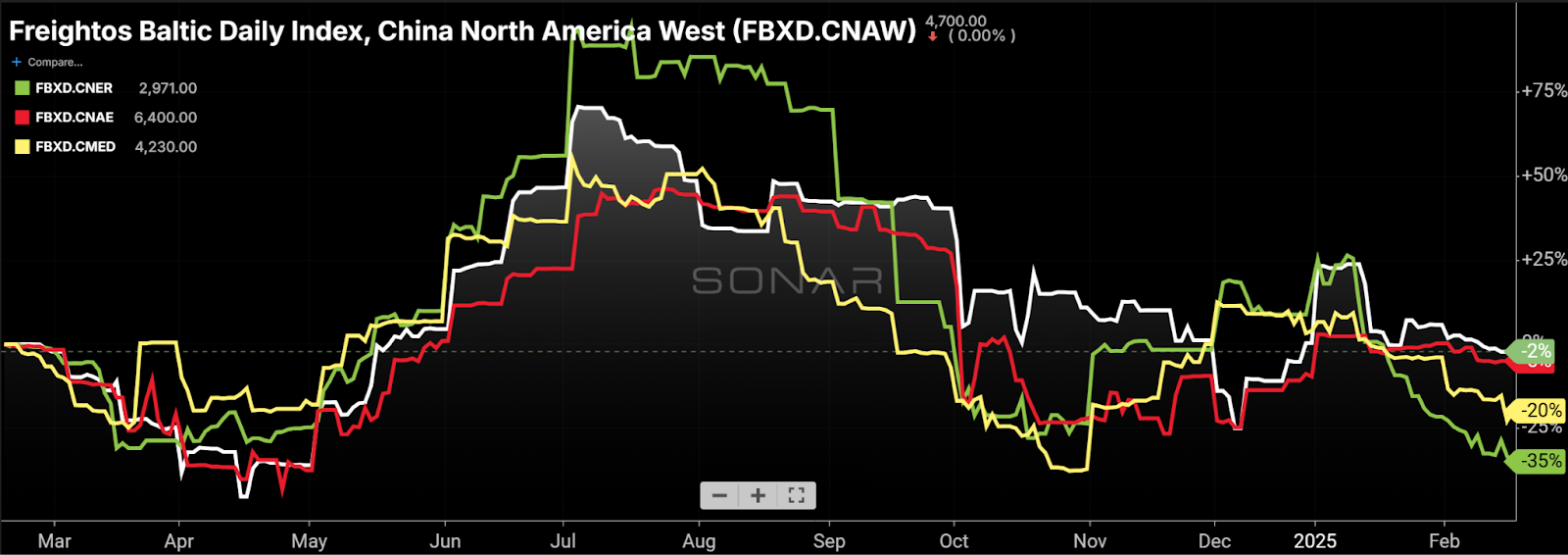

Likely reflecting a demand pull-forward, ocean rates from China to the U.S. have held up much better than those from China to other regions. The one-year changes in ocean rates from China to the U.S. West Coast and U.S. East Coast are shown in white and red, respectively. Over the same period, ocean rates from China to the Mediterranean (yellow) and North Europe (green) are down 20% and 35%, respectively. (Chart: SONAR)

The Stockout Show

(Image: FWTV)

On Monday’s The Stockout show, I provided an update to the discussion on the show the prior two weeks describing the impact that tariffs are likely to have on the consumer packaged goods and retail industries. In addition, I discussed the consumer economy and several freight transportation sectors.

The container ship sector is one area that has the potential for volatility this year. The reduced potential for additional attacks in the Red Sea may cause the remaining carriers to reenter the region, which would increase the effective capacity by 8%-10%. At the same time, shipbuilders fulfilling orders placed during the boom years during the pandemic could increase capacity by 8% this year. Meanwhile, the pull-forward of ocean shipping volume the past several months ahead of tariffs could lead to a drop in demand later this year. As a result, carriers may have to increase the quantity of blank sailings in an effort to stabilize rates which, while off their highs, remain elevated compared to historic norms.

See the full The Stockout playlist here.

We have a new FreightWaves group for you to check out!

The Playbook: Your Roadmap to Success in Trucking

Small carriers and owner-operators often struggle with fragmented, outdated or wrong information. That’s where The Playbook comes in. Built by Adam Wingfield — a 22-year trucking industry veteran — it’s the comprehensive resource you’ve been waiting for.

Why The Playbook?

After years of seeing small carriers struggle, Wingfield teamed up with FreightWaves to create a structured, fact-based guide to succeed in trucking. The Playbook is not just another content hub — it’s a one-stop resource for success.

What’s inside?

- Roadmap Digital Learning Hub: Step-by-step courses and training on compliance, finance, operations and sales.

- Masterclass: Biweekly sessions diving deep into the key areas of trucking business growth

- The Long Haul Podcast: Insights from industry experts on growing your trucking business.

- Partner Portal: Connect with vetted industry partners and grow your business efficiently.

- Small Carrier Market Update: Stay ahead with real-time freight trends and insights.

- Tools & Templates: Access spreadsheets, calculators and contract templates.

Why FreightWaves?

FreightWaves brings industry-leading data and analytics to the table, ensuring you get the same insights larger carriers rely on.

The Playbook’s mission

It’s not just a project — it’s a movement to ensure small carriers thrive in an industry where knowledge is power.Sign up for the weekly Playbook newsletter here.

The post Another year of stagnant intermodal pricing? appeared first on FreightWaves.