Venture capital prepares to ignite stores of dry powder

The story of venture capital in 2024 was one of resilience and green shoots, but also one of hype in which the big fish ate the little ones. The post Venture capital prepares to ignite stores of dry powder appeared first on FreightWaves.

This article is the first of three on the landscape of venture capital and FreightTech in 2025 and beyond.

Falling from the heights of the 2021-22 boom — when near-zero interest rates made for essentially free money — the past few years have been rough for venture capital.

Hugh MacArthur, chairman of Global Private Equity at Bain & Co. and founder of its annual “Global Private Equity Report,” opened last year’s report by declaring that “the year 2023 was one of portent.

“Deal value fell by 37%,” MacArthur continued. “Exit value slid even more, by 44%. … The word for this market is stalled.”

The report went on to forecast that VC would see the early stages of a recovery in 2024 — which it did, aided in large part by the proliferation of AI startups. VC deal values rose from $162.2 billion in 2023 to $209 billion in 2024, per PitchBook. The number of deals grew likewise, from 14,712 to 15,260.

Despite this promising growth, something was rotten in the state of VC.

For one, 30% of 2024’s deals involved flat or down rounds: an abnormally high share, even when looking beyond the recent boom. VC fundraising was at its lowest since 2019. Of the $76.1 billion raised, the top nine firms captured nearly half.

Consolidation was also seen at the other end of the table. Of the $74.6 billion in deal value during the fourth quarter, 43% came from just five deals: Databricks, OpenAI, xAI, Waymo and Anthropic. Unsurprisingly, these companies are all major participants in the AI gold rush.

The story of VC in 2024 was thus one of resilience and green shoots, but also one of hype in which the big fish ate the little ones.

2025: Cloudy with a chance of recovery

With such a mixed performance in the rearview mirror, what is to become of 2025?

The consensus is one of cautious and conditional optimism, based primarily on the expectation that exit activity will ramp up in 2025, freeing the liquidity necessary to revitalize the VC space.

Exits — whether startups are acquired by another company for cash and/or stock or, in many founders’ dream scenarios, they go public after a stock launch — have been impeded by a variety of factors over the past three years.

Most obviously (and most culpably), near-zero interest rates shot up in early 2022 to two-decade highs over 5%, following Russia’s invasion of Ukraine and the ensuing rally in energy prices. It goes without saying that a higher cost of borrowing deters capital expenditures like acquisitions.

The path back down has been rocky and uneven. Inflation has proved intractable: With consumer prices up 3% in January, inflation is far beyond the Federal Reserve’s target of 2% yearly growth.

Despite this persistent issue, the Fed rushed to cut rates by a cumulative 100 basis points at three consecutive meetings in late 2024, which helps to explain Q4’s rise in VC deal value. The reasoning behind these cuts was rather thin, especially coming from the avowedly data-dependent Fed under Chair Jerome Powell. No substantial indications had been given that inflation was tamed, but — looking at the other half of the Fed’s dual mandate — the labor market was not yet grim enough to warrant such intervention.

Any predictions on what the Fed will do in 2025 are necessarily tethered to how consumer prices will react (if indeed they will) under President Donald Trump’s unpredictable, tariff-heavy trade policy. For its part, PitchBook is relatively assured that the fight against inflation will proceed favorably, though it takes care to note the risks inherent to this prediction.

Bain reaffirms this cautious optimism in its most recent “Global Private Equity Report”: “Whether the momentum can build in 2025 will largely depend on macro conditions and policy. … [T]he year’s early slowdown in M&A activity globally suggests that the dreaded U word (uncertainty) continues to keep markets on edge.”

The Fed stands unenviably at a crossroads. If tariffs proceed to have a meaningful impact on consumer prices, then the central bank is charged with maintaining high interest rates until inflation subsides.

Yet if the current environment of quantitative tightness persists much longer, the labor market might threaten to collapse. A spike in unemployment would signal a recession, at which point the Fed would be pressed to slash rates as quickly as possible.

At present, the Fed is likely to continue its hawkish pause at its meeting on Mar. 19. Though slightly weaker than expected, February’s payroll data portrayed a mostly stable labor market that does not require immediate rate cuts.

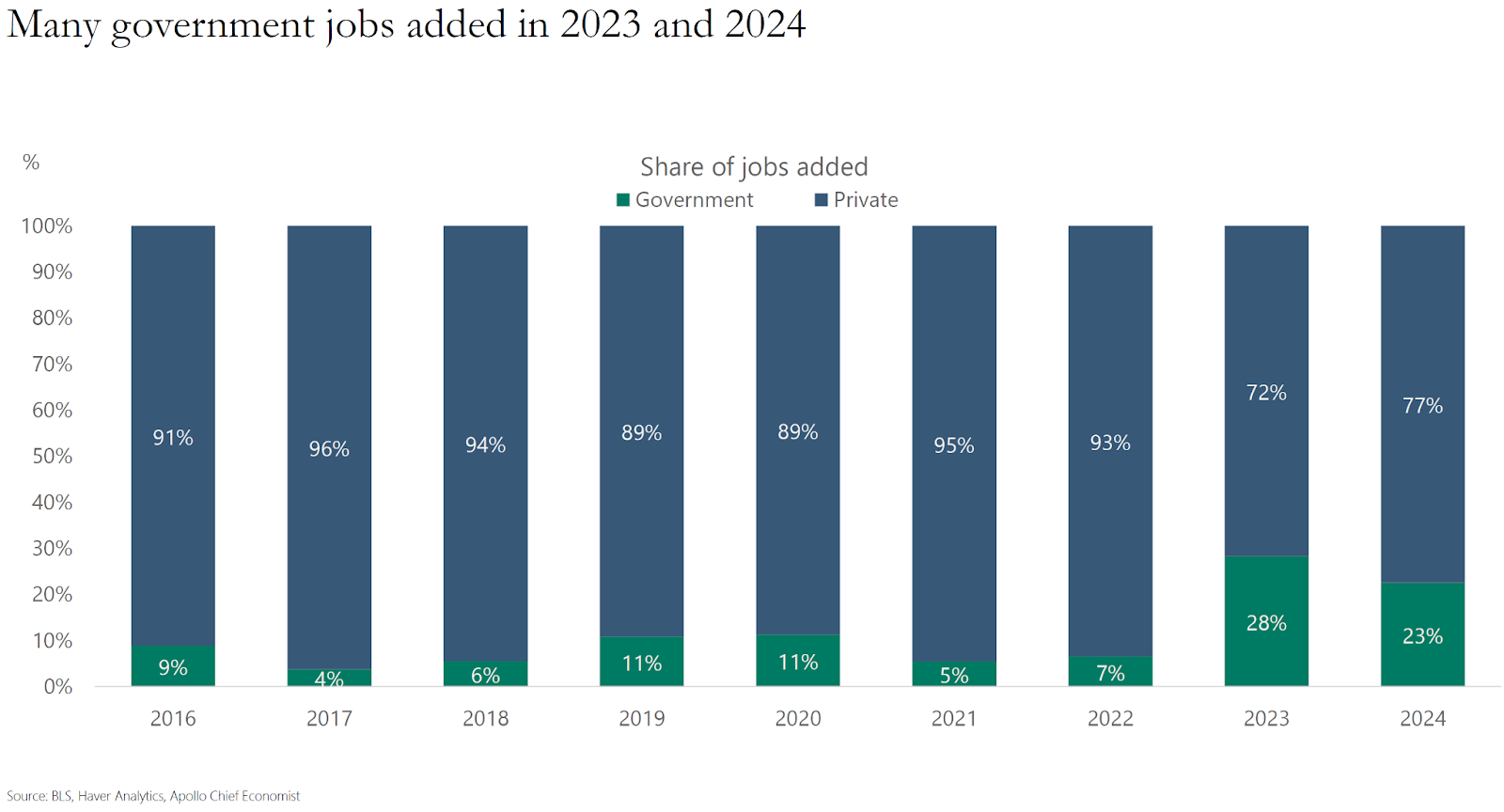

How the labor market will fare in the rest of 2025 is an open question, however. Government positions accounted for roughly a quarter of the total jobs added in 2023 and 2024, far higher than the 7% share in 2022 and 5% in 2021. The current administration, with the newly created Department of Government Efficiency (DOGE), aims to reduce the national deficit by trimming the federal workforce.

Apollo Global Management forecasts that DOGE’s layoffs will cause total U.S. unemployment to rise by less than 1 million from baseline, which is itself around 7 million. Considering that total employment is 160 million, Apollo argues, DOGE’s cost-cutting measures will have a noticeable but not devastating impact on the labor market.

The consensus outlook for 2025 therefore sees VC as being unaided by any surprise tailwinds from the Fed, which is on course to remain hawkish in the few cuts it allots.

The post Venture capital prepares to ignite stores of dry powder appeared first on FreightWaves.